A risk assessment for Ontarians

Canadian Centre for Economic Analysis Inc.

Copyright © 2017 All rights reserved.

Technical questions should be directed to connect@cancea.ca

Download original document [PDF]

CANCEA

- In July 2017, the Ontario Chamber of Commerce along with the Keep Ontario Working Coalition awarded CANCEA the challenge of measuring the potential impacts of the six key areas of change in the proposed Fair Workplaces, Better Jobs Act, 2017 (the Act). CANCEA is known for it objective reporting of the risks and rewards of policy and market strategies and has government work experience in Ontario:

- Ministry of Finance, Ministry of Infrastructure, Treasury Board, Ministry of Community and Social Services, Canadian Mortgage and Housing Corporation, City of Toronto, Region of Peel, City of Hamilton

- CANCEA team:

- Paul Smetanin MQF, B.Econ, CA. : Expertise in economic policy, behavioural economics, demographics, risk management and measurement approaches

- David Stiff Ph.D, B.Eng. : Expertise in numerical simulations of complex systems, applications to the fields of economic policy, risk management and demographics

- Tasos Papanastasiou Ph.D, M.A (Econ), B.Econ: Expertise in microeconomic theory, econometrics, game theory

- Sener Salci Ph.D, M.Sc (Econ), B.Sc (Econ): Expertise in applied welfare analysis, applied microeconomics

- Aaron Zhu Ph.D, B.Eng: Expertise in data science, machine learning, predictive modeling, model selection.

- CANCEA does not accept any research funding or client engagements that require a pre-determined result or policy stance, or otherwise inhibits its independence.

- In keeping with CANCEA’s guidelines for funded research, the design and method of research, as well as the content of this study, were determined solely by CANCEA.

- This information is not intended as specific investment, accounting, legal or tax advice.

Analysis and Presentation

This presentation serves to release the key results of the analysis under an expedited process:

- There are many more results to be reported in detail that shows how the expected outcomes transpire and for whom they affect

- A full report will be forthcoming later in August 2017

Given the nature of the Act the analysis of its impacts represents an exercise in measuring risks and rewards for different Ontario stakeholders and understanding the potential for unintended consequences.

The analysis is achieved through the use of :

- Detailed Ontario demographic, economic and financial data (primarily from Statistics Canada)

- Reasonable interpretations of the leading economic literature in the field (low end estimates of different impacts have been preferred)

- Modern computer modelling of the accounting behind firms, households, consumers and governments

All technical questions should be directed to connect@cancea.ca

Ontario Prosperity and the Act

- Themes of minimum wage increases, equal pay and the general sharing of economic prosperity are congruent to most peoples’ wishes in a competitive mixed market economy such as Ontario and Canada

- Significant economic and societal structural changes have occurred over the decades

- CANCEA has analyzed and written about such issues before

- Fair Workplaces, Better Jobs Act, 2017 (the Act) could be viewed as an attempt to address such themes and structural changes

- The analysis is an evidenced-based, agenda-free accounting of the economic risks and rewards of the Act for Ontarians and the businesses that they rely upon

Results at a Glance

Fair Workplaces, Better Jobs Act, 2017 is expected to:

- Increase the risks and uncertainties for many Ontario business sectors

- Significance: Ontario businesses will need to adjust to at least one of 64 different labour cost outcomes

- Suddenness: 15 month period with added ambiguity yet to be resolved or tested

- Size: minimum wage changes scheduled largest in 45 years, being 15 times the average

- Create a $23B challenge for Ontario businesses in just the first 2 years: $10.2B (2018), $13B (2019). Putting this into perspective, the amount in play represents:

- 21% of Ontario private business investment each year (excl. res construction)

- 100% of the corporate tax revenues paid to the Ontario government each year

- About 185,000 jobs are expected to be at risk over the coming years representing about 2.4% of all employees

- Based upon the expected behaviour of Ontario businesses: 50% of costs reduced through employment changes, 21% absorbed by business, 29% passed onto consumers (0.7%increase)

- Have different impacts for different firms in different locations. Owners of small businesses are likely to be affected five times more than larger businesses

- Affect women more than men

- While a greater percentage of the young will feel the job risk, 83% of the expected jobs at risk are for ages of 25yrs and over

- If the 3 levels of governments absorb the 100% of costs, then

- Federal government: Additional revenue of $500M – costs of $610M yields a net loss of $110M

- Provincial government: Additional revenue of $620M – costs of $1.1B yields a net loss of $440M

- Municipalities: Net loss of $500M with no additional revenue (property taxes?)

Breakdown of the Expected Jobs at Risk

Of the expected 185,000 jobs at risk:

- The jobs at risk includes both current and potential new jobs. While the population grows we expect the number of jobs to be 2.4% below what it could have been. This is what is meant by jobs at risk.

- A bulk of the risks come in the form of:

- Firms repurposing and repackaging their labour requirements towards

- Getting more out of less employees (search for labour productivity benefits)

- Reduced new hiring

- Taking advantage of opportunities to substitute labour for technology and process improvements

- Firms reducing their plans for private capital investment (ie. not scaling up as much as expected)

- Firms repurposing and repackaging their labour requirements towards

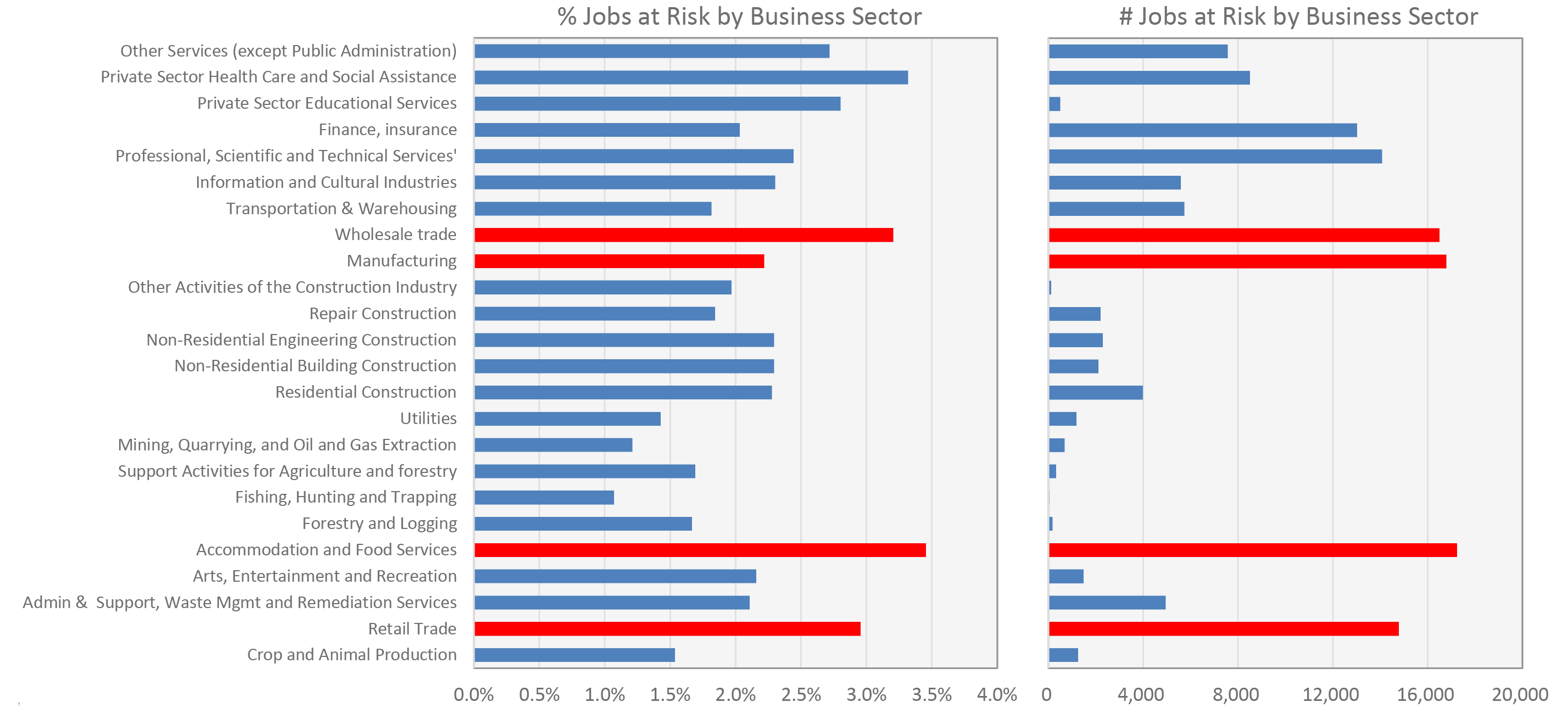

Results: Sectors at Risk

Dissecting the $23B, and using the expected scenario of 185,000 jobs at risk, the impacts are not uniformly felt across sectors. At highest risk are:

- Manufacturing (16,800 jobs),

- Accommodation and food services(17,300 jobs) and

- Retail trades (14,700 jobs)

- Wholesale trades (16,000 jobs)

Results: Employees at Risk

Dissecting the $23B, and using the expected scenario of 185,000 jobs at risk, the employee cohorts breakdown is:

- Under 25 years are affected 1.15 more times than older age groups

- 17% of the expected job losses

- About 30,000 jobs at risk or a 3.0% reduction in employment percentage

- Over 25 years to 55 years represent:

- 63% of the expected job losses

- About 116,000 jobs at risk or a 2.6% reduction in employment percentage

- Over 55 years represent:

- 20% of the expected job losses

- About 38,000 jobs at risk or a 2.6% reduction in employment percentage

- Men and women represent:

- 52% of the expected job losses are expected to be women

- About 96,000 jobs at risk for women (2.8%) and 89,000 jobs at risk for men (2.5%)

Results: Firm Size

Dissecting the $23B, and using the expected scenario of 185,000 jobs at risk, the firm size breakdown is:

- Firms less than 20 employees

- The number of jobs at risk is equivalent to over 5,000 firms of this size.

- Firms less greater than 20 employees and less than 100

- The number of jobs at risk is equivalent to over 1,000 firms of this size

- Firms greater than 100 employees

- The number of jobs at risk is equivalent to about 400 firms of this size

- Five times more owners of small businesses with fewer than 20 employees may be affected than larger businesses

Results: Consumer Prices

Dissecting the $23B, and using the expected scenario of 185,000 jobs at risk:

- Consumer price changes will vary across business sectors

- Consumer prices are expected to increase by a further 0.7% on average

- This translates into an additional increase of consumer goods and services by $1,300 per household on average per annum.

Results: Fiscal Revenues

Dissecting the $23B, and using the expected scenario of 185,000 jobs at risk:

- The Ontario government could be expected to net an additional $620M annually in tax revenue due to:

- Greater personal income tax revenue

- Greater consumer spending and consumption tax revenue, and

- Reduced corporate tax revenue

- The federal government could to net an additional $500M annually

However, the 3 levels of governments would also have to redistribute the costs resulting from higher wages. If governments absorb the 100% of costs, then

- Federal government:

- Additional costs of $0.61B yields a net loss of $0.11B if government

- Provincial government:

- Additional costs of $1.1B yields a net loss of $0.44B

- Municipalities:

- Net loss of $0.5B with no additional revenue

If governments absorb 52% of the additional costs (with the remainder accounted for through reduced employees and passing costs on for services), governments (on aggregate) break even

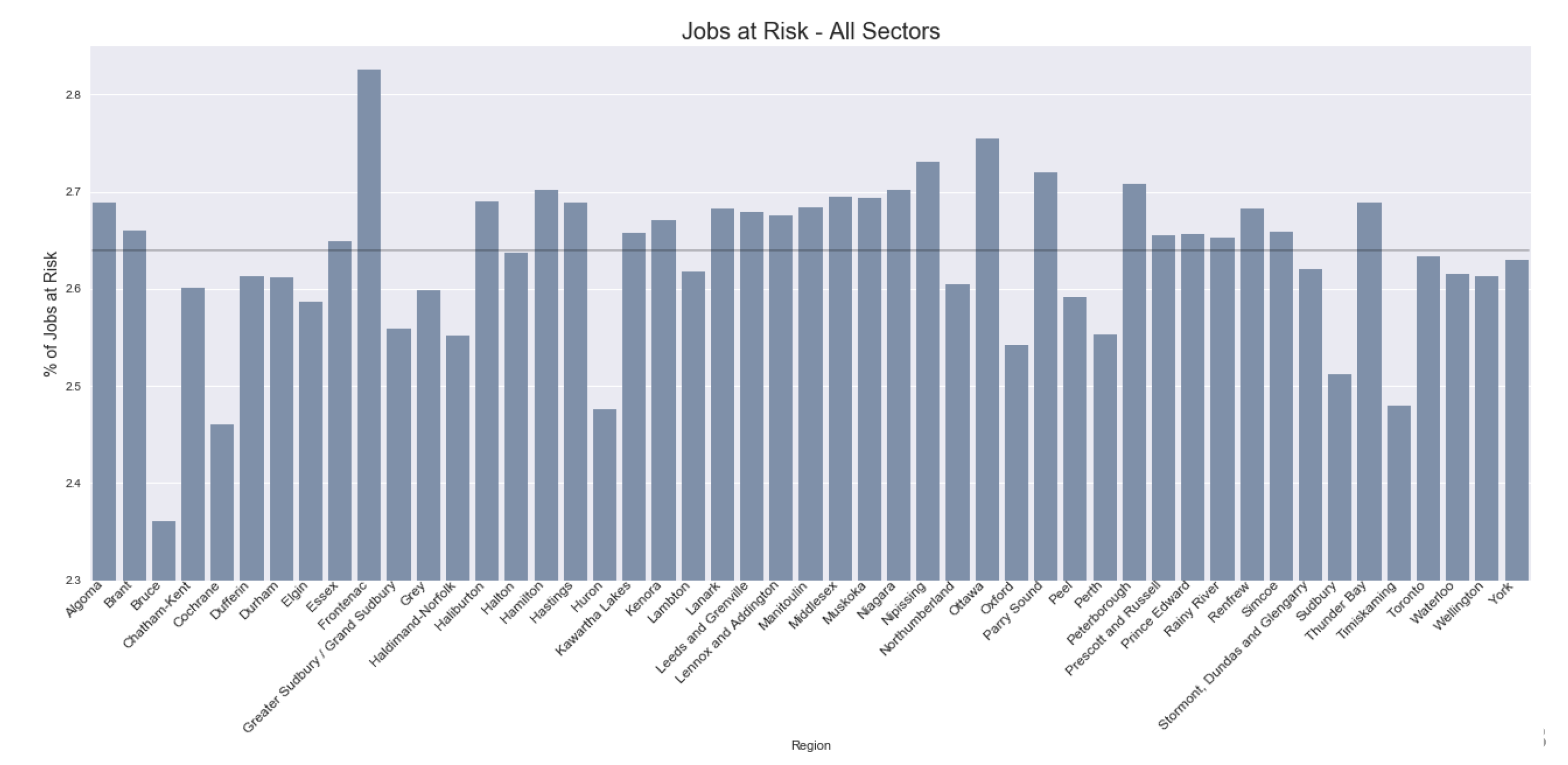

Results: Regional

The analysis also highlights the discrepancy between regions

- The Act will not affect all regions of the province equally with some regions having 20% greater share of their local jobs at risk than others

The jobs at risk depend significantly on the industries and demographics of each area

Appendix

Methodology Overview

- For any firm, the value of the outputs must balance the value of the inputs when inputs include:

- Intermediate goods and services (as required by the output quantity demanded by consumers and other industry using input/output tables)

- Net taxes on products and production

- Total wages which is the product of number of employees, hours worked per employee, and hourly wages (modelled by age, sex, full/part time, sector, and unionization status)

- Gross operating surplus (possibly negative)

- An increase in hourly wages creates an imbalance which must be redistributed to maintain the equality. This can be achieved (while maintaining the same output volume) by firms:

- Decreasing gross operating margins,

- Decreasing the number of employees through productivity changes, or

- Increasing the unit price of outputs

- The response by firms varies by sectors as different sectors have different business models and bargaining power (ability to make changes). For example, we have assumed that the public sector will not reduce labour cost impacts, but will raise debt levels and ultimately pass on the costs to Ontario taxpayers

- The net change in household disposable income (could be positive or negative depending on firms’ responses) results in a change in consumer consumption patterns

- This change in demand feeds back into industry demand

- Despite economic evidence to the contrary, the current results have not been adjusted for expected changes in the private capital investment plans of firms that operate in Ontario. Such an adjustment would result in worse outcomes reported here.

- The results are most sensitive to minimum wage changes and assumptions around equal wage provisions.

Assumptions Behind the $23B Challenge

The proposed changes behind the Act generally represents an attempted redistribution from Ontario business income and wealth to employees. There are uncertainties behind the exact figure, however, the following assumptions are used and are considered reasonable:

- Minimum Wage Increase: less than $15 to $15 per hour for about 1.5 million employees and a wage ripple effect for those about $15 consistent with the analysis of Campolieti (2015)

- Equal Pay Provisions: Alignment of all average wage rates by using current public sector experience (general average increase of 3% which differs by age, sex, and sector)

- PEL: Businesses less that 50 people lose 2 days per annual of productivity and wage. Businesses greater than 50 employees lose 2 days per year of wage only.

- Vacation: Same PEL approach used for vacation adjusting for tenure.

- Labour Overhead: 1% of part-time wages under the assumption that 50% of the change is recouped by substitution or repurposing of labour (net 0.5% change)

- Unionization: One time increase of 2% of rate of unionization with wages to match by age and sex for 2018 returning to unionization rates of the early 1990s.

Note: the results are very sensitive around assumptions of the minimum wage changes, the ripple effect and equal pay changes (likely resolved through a variety of different responses across sectors and wage scales)