Table of Contents

- Overview

- Executive Summary

- Canada’s Economy: One Step Forward, Two Steps Back

- Commodity Prices: Oil Is Headed Lower in 2016

- China: Slowdown to Continue, But No Hard Landing

- The Canadian Dollar: Weaker in 2016, But Picking up in 2017

- The Bottom Line for Canadian Business

- The Crystal Ball Symposium: The Biggest Challenges Facing Canada and the Global Economy

- Critical Issues in the Years Ahead: Are Robots a Real Threat to Employment?

- Rising Political Risk: Migration, Terrorism and the Business Risk Calculus

Overview

The Crystal Ball Report examines the most significant economic, political and technological issues facing Canadian business in order to forecast critical opportunities and challenges in the years ahead. This report is the culmination of extensive research and input from businesses across Canada and from the global experts who helped us gaze into the crystal ball.

Throughout 2015, the Canadian Chamber of Commerce hosted a series of thought leadership roundtables, a unique gathering of Canadian businesses from every sector of the economy to talk about the big issues—energy and commodity prices, the digital economy, international trade, risks—and their priorities in the years ahead. In the autumn, the Canadian Chamber interviewed three outstanding economists, Peter Hall, Vice President and Chief Economist of Export Development Canada, Mark Zandi, Chief Economist at Moody’s Analytics, and Barry Eichengreen, George C. Pardee and Helen N. Pardee Professor of Economics and Professor of Political Science at the University of California Berkeley and author of dozens of books. At the end of the year, the Canadian Chamber hosted its Crystal Ball Symposium, inviting global thought leaders to join with Canadian businesses and public servants to talk about two important issues: the future of work in an era of rapid technological progress and the future of the world in the face of political instability and terrorism.

Armed with the insights and commentaries of business experts and top public servants, the Canadian Chamber has prepared its annual forecast report.

Thought Leadership Across Canada

Date |

City |

Topic |

|---|---|---|

| January 15, 2015 | Calgary | Economic Outlook |

| April 14, 2015 | Ottawa | Industry Association Roundtable |

| May 20, 2015 | Calgary | Election 2015 |

| July 6, 2015 | Vancouver | Access to World Markets |

| September 21, 2015 | Saskatoon | Access to World Markets |

| September 23, 2015 | Toronto | The Future of Data Privacy in the Digital Economy |

| September 28, 2015 | Ottawa | Industry Association Roundtable |

| October 27, 2015 | Vancouver | Duty to Consult |

| November 3, 2015 | Calgary | Post Federal Election and Outlook for Canada |

| November 10, 2015 | Toronto | Getting Immigration Right |

| November 12, 2015 | Yellowknife | Duty to Consult |

| November 24, 2015 | Winnipeg | Trade-enabling Infrastructure and Access to Markets |

| November 30, 2015 | Ottawa | Crystal Ball Symposium: The Future of Work and Technology, Global Migration and Terrorism |

Executive Summary

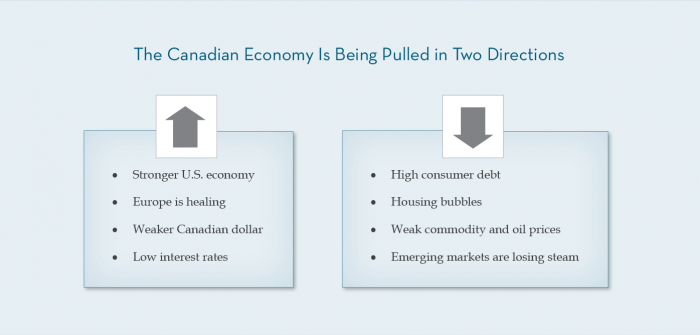

The Canadian business community is deeply divided in its outlook for 2016-2017 between optimism in sectors that are experiencing rapid growth, such as forestry, automotive and technology, and gloom in the mining and energy sectors stricken by low commodity prices. On the global economy, business expressed enthusiasm for prospects in the U.S., where the economy is poised for impressive growth in 2016, and in Europe, which is accelerating. However, there are continued worries about emerging markets, particularly China, which are likely to disappoint this year. As a result, commodity prices will remain weak at least until 2017. Lastly, there was a great deal of apprehension about Canada’s domestic economy.

A participant at one of the roundtables commented, “Where is growth going to come from? Not consumption—the consumer is tapped out. Government spending can’t provide much lift. Although the feds can spend more, the provinces are mostly in cut-back mode. We can’t rely on natural resources anymore and housing is overbuilt. That leaves exporting goods and services. So we’d better start exporting like crazy.”

Canada must compete and succeed in a challenging global economy with huge gyrations in commodity prices, currencies and stock markets happening around the world. Competitiveness has become even more critical to our growth and prosperity. According to the business leaders we consulted, in order to improve Canada’s competitiveness, the following issues must be addressed in 2016-2017:

- Skills and labour: Canadian business is facing skills gaps and mismatches right across the board. There is an urgent need for new immigrants and for skills and education that are aligned with the needs of employers.

- Infrastructure: Strategic investments in infrastructure can make Canada more competitive, bring down costs and help get our goods to market. Business leaders emphasized that the priority has to be placed on trade-enabling infrastructure that will improve productivity.

- Environment and consultations: For years, Canadian business and the Canadian Chamber have called for a coherent plan to improve the environment and reduce green house gases without damaging Canada’s competitive position. There is a recognition that improved energy efficiency and green technology can be a source of competitive advantage. In addition, a stronger federal role is needed in consultations and outreach with First Nations and local communities.

- Innovation and the digital economy: Canada must support more start-ups, attract more venture capital and provide more incentives to commercialize new technologies right here at home.

- Trade and regulatory harmonization: Canada must move quickly to ratify the Trans-Pacific Partnership and the Canada-Europe Trade Agreement. For many industries in the knowledge economy, regulations, ownership requirements and restrictions on data fl ows can be the most difficult barriers to success. This issue must be a global priority for the Canadian government and for the G20.

CANADA’S ECONOMY: ONE STEP FORWARD, TWO STEPS BACK

The Canadian economy is facing significant challenges in the years ahead. We emerged from recession in the third quarter of 2015 with a healthy growth of 2.3%, but many of the headwinds will worsen as we move into 2016.

The main reason for moderating growth is a slowdown on the consumer side. Consumption is 70% of Canada’s GDP, so it matters very much how Canadians are feeling and whether they are spending. Job and wage growth will be very soft in 2016 as weakness in the oil patch and natural resource industries offsets rosier growth in manufacturing and services.

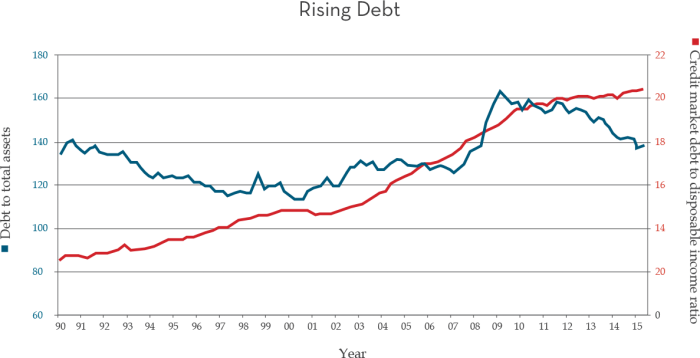

Worse, Canadians are struggling with high levels of debt, now at a record high of 164% of disposable income. The CD Howe Institute reports that 11% of Canadian households have mortgage debt that is more than 500% of their disposable income and will experience financial distress when interest rates rise. This same study shows how vulnerable we are: 20% of households have less than $5,000 available to deal with a job loss or an emergency, and 10% of households have less than $1,500.

The following graph shows that despite increased borrowing, the debt-to-asset ratio continues to fall, a sign of rising wealth in Canada. Asset values continued to increase faster than liabilities despite a weak performance by Canadian stocks.

“Smart companies should consider moves into new markets now while competitors are still sitting on the fence, particularly in the U.S., and ahead of the new competition that will be coming in a few years’ time from free trade agreements with the European Union and Pacific Rim countries.”

Peter Hall,

Vice President and Chief Economist,

Export Development Canada

However, the bulk of growth in asset prices is in real estate. The Bank of Canada warns that homes are 10-30% overvalued, while the Canada Mortgage and Housing Corporation warns that 15 out of Canada’s 17 largest cities are showing signs of bubbly prices. This is so alarming to the government that one of the first actions of the new Finance Minister was to raise the down payment required for mortgage amounts exceeding $500,000 from 5% to 10%. Consumer vulnerability is a significant risk to the Canadian economy.

With consumer confidence weak in many parts of Canada, retail sales will be softer in 2016. More than in the past, Canadian businesses told us that they have to look outside of Canada if they want to achieve rapid growth.

Featured Economists

Peter G. Hall

Peter G. Hall

Vice President and Chief Economist, Export Development Canada

Peter Hall joined Export Development Canada (EDC) in November 2004. With over 25 years of experience in economic analysis and forecasting, Mr. Hall is responsible for overseeing EDC’s economic and political risk analysis, special research and the corporate library. In addition to advising senior management at EDC, Mr. Hall is a featured speaker at conferences, international roundtables and policy fora and regularly appears in television, radio and print media commenting on the international economy.

Prior to joining EDC, Mr. Hall directed the economic forecasting activities of the Conference Board of Canada. Mr. Hall serves on the boards of the Canadian Association for Business Economics and its local Ottawa chapter.

Mr. Hall is the immediate past president of the Canadian Association for Business Economics, a 600-member national association of professional economists, and actively participates in its local Ottawa chapter. Mr. Hall has degrees in economics from Carleton University and the University of Toronto.

Barry Eichengreen

Barry Eichengreen

George C. Pardee and Helen N. Pardee Professor of Economics and Political Science, University of California, Berkeley

Barry Eichengreen is the George C. Pardee and Helen N. Pardee Professor of Economics and Professor of Political Science at the University of California, Berkeley, where he has taught since 1987. He is a Research Associate of the National Bureau of Economic Research (Cambridge, Massachusetts) and Research Fellow of the Centre for Economic Policy Research (London, England). In 1997-98 he was Senior Policy Advisor at the International Monetary Fund. He is a fellow of the American Academy of Arts and Sciences (class of 1997). Professor Eichengreen is the convener of the Bellagio Group of academics and economic officials and Chair of the Academic Advisory Committee of the Peterson Institute of International Economics. He has held Guggenheim and Fulbright Fellowships and has been a fellow of the Center for Advanced Study in the Behavioral Sciences (Palo Alto) and the Institute for Advanced Study (Berlin).

Professor Eichengreen is a regular monthly columnist for Project Syndicate and is the author of many books on the global economy.

Professor Eichengreen was awarded the Economic History Association’s Jonathan R.T. Hughes Prize for Excellence in Teaching in 2002 and the University of California at Berkeley Social Science Division’s Distinguished Teaching Award in 2004. He is also the recipient of a doctor honoris causa from the American University in Paris.

Mark Zandi

Mark Zandi

Chief Economist, Moody’s Analytics

Mark M. Zandi is Chief Economist of Moody’s Analytics, where he directs economic research. Moody’s Analytics, a subsidiary of Moody’s Corp., is a leading provider of economic research, data and analytical tools. Dr. Zandi is a cofounder of Economy.com, which Moody’s purchased in 2005.

Dr. Zandi’s broad research interests encompass macroeconomics, financial markets and public policy. His recent research has focused on mortgage finance reform and the determinants of mortgage foreclosure and personal bankruptcy. He has analyzed the economic impact of various tax and government spending policies and assessed the appropriate monetary policy response to bubbles in asset markets.

A trusted adviser to policymakers and an influential source of economic analysis for businesses, journalists and the public, Dr. Zandi frequently testifies before Congress on topics including the economic outlook, the nation’s daunting fiscal challenges, the merits of fiscal stimulus, financial regulatory reform and foreclosure mitigation.

Dr. Zandi conducts regular briefings on the economy for corporate boards, trade associations and policymakers at all levels. He is on the board of directors of MGIC, the nation’s largest private mortgage insurance company, and The Reinvestment Fund, a large CDFI that makes investments in disadvantaged neighbourhoods. He is often quoted in national and global publications and interviewed by major news media outlets. He is a frequent guest on CNBC, NPR, Meet the Press, CNN, and various other national networks and news programs.

Dr. Zandi is the author of Paying the Price: Ending the Great Recession and Beginning a New American Century, which provides an assessment of the monetary and fiscal policy response to the great recession. His other book, Financial Shock: A 360° Look at the Subprime Mortgage Implosion, and How to Avoid the Next Financial Crisis, is described by the New York Times as the “clearest guide” to the nancial crisis.

Dr. Zandi earned his B.S. from the Wharton School at the University of Pennsylvania and his PhD at the University of Pennsylvania. He lives with his wife and three children in the suburbs of Philadelphia.

“American consumers are sturdy thanks to solid job growth, rising real wages, restored confidence, better-managed household budgets and a $100 billion bonus from lower gasoline prices.”

Peter Hall,

Vice President and Chief Economist,

Export Development Canada

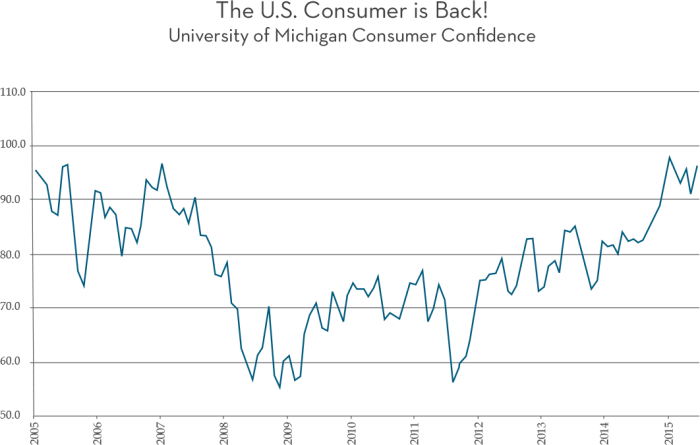

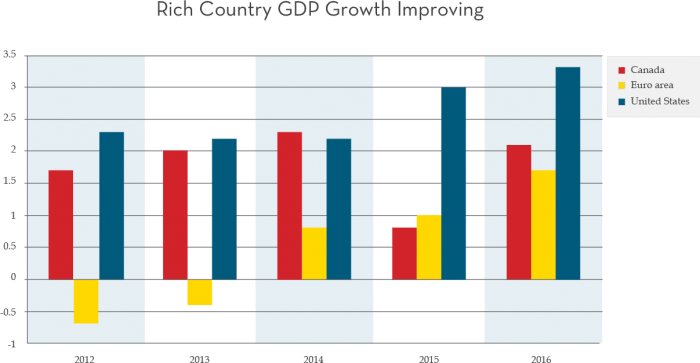

Seven years after the great recession, the world’s richest countries are finally getting back to a position of strength. The U.S. economy is expected to grow 3.1% in 2016 and 2.7% in 2017, strong enough that the U.S. Federal Reserve felt it had no choice but to raise interest rates.

The U.S. consumer is back with a vengeance, spending and borrowing with enthusiasm not seen since before the great recession. With unemployment down to just 5%, the majority of Americans feel more secure in their jobs.

“The U.S. economy is performing well. Corporate profits are solid, and the job market is booming. The economy will be running at full capacity by mid-2016, and, at that point, wages will really start to pick up.”

Mark Zandi,

Chief Economist, Moody’s Analytics

The business sector is also performing well. Corporate profits have weakened slightly, a consequence of a higher U.S. dollar squeezing profits and competitiveness. However, businesses are also holding around $6 trillion of cash, the most liquid balance sheets since the 1950s.

U.S. capacity utilization is almost back to its pre-crisis peak, and productivity gains are trailing off. If a business wants to increase production, it has little choice but to invest in new equipment and hiring. U.S. business investment has been picking up impressively, and corporations have enormous resources to deploy, so we can look forward to rising trends in business investment. The economies of Europe are also gaining strength and are expected to grow 1.5% in 2016. We estimate that Europe’s fastest growing economy will be either Spain or Ireland, as the south finally gets back on track. At the same time, Japan will grow by 1.5% as deflation is averted thanks to aggressive action from the government.

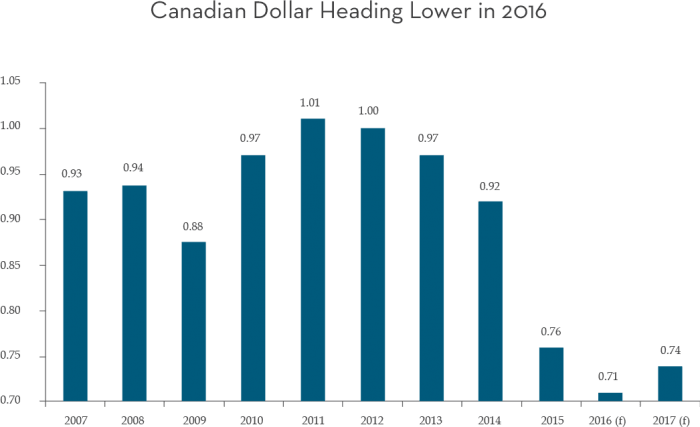

This means our largest trading partners are gaining strength while the Canadian dollar will hit record lows. The Canadian dollar is expected to average $0.71 in 2016—a healthy boost for exporters.

COMMODITY PRICES: OIL IS HEADED LOWER IN 2016

One of the biggest concerns of Canadian business is the outlook for oil and commodity prices. The research and interviews we have undertaken have led us to believe that the biggest drag on the Canadian economy will be low commodity prices, which are expected to persist through 2016 and 2017.

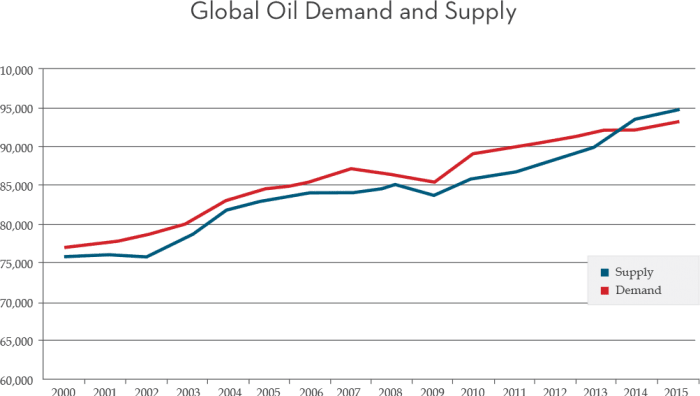

Oil markets are in turmoil: there is excess production of approximately 1.5 million barrels per day; the price of oil is fluctuating in the $30 range; the U.S. is poised to end its 40-year-old export ban and the Organization of Petroleum Exporting Countries (OPEC) cartel has essentially given up on controlling production.

By the end of 2015, global oil markets had about the same level of excess supply as at the end of 2014, which was a surprise to most oil analysts. The expectation was that oil markets would return to balance because of the big demand response following a 60% fall in price. Indeed, the International Energy Agency (IEA) points out that global oil demand rose by 1.8 million barrels per day, which is signicant, but still well below the 2.5-3 million barrels per day growth seen in past years. The trouble is that emerging markets, the sources of the biggest demand growth, have been disappointingly weak, and the IEA expects global demand growth to fall to 1.2 million barrels per day in 2016.

“It’s difficult to see why oil prices would pick up in 2016. There is just not enough demand to absorb the production oversupply.”

Mark Zandi, Chief Economist,

Moody’s Analytics

At the same time that demand growth is slowing, oil markets will be afflicted by oversupply thanks to rising production from OPEC. At its meeting in November, OPEC abandoned its (soft) cap of 30 million barrels per day.

In 2016, Iran by itself could add 500,000 barrels per day once sanctions are lifted. The prospects of future OPEC agreements to restrict production are poor. Countries like Iraq, Venezuela and Nigeria are in such dire financial straits that they simply cannot afford reductions and will be selling as much as possible.

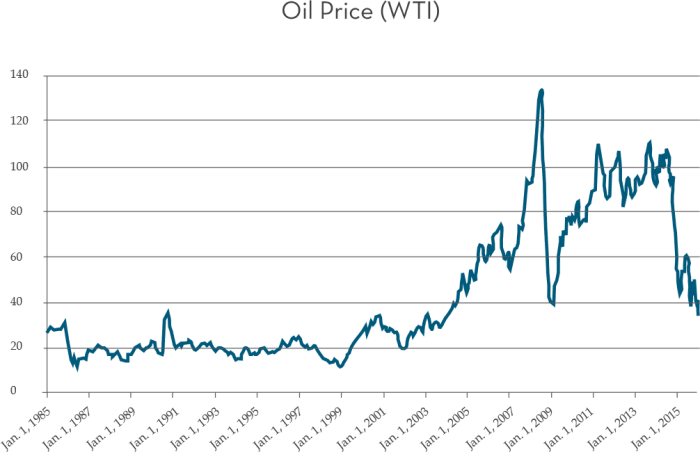

This is why we are forecasting that oil prices will average $35 through 2016 before rising to the $55 range in 2017. The biggest challenge in oil forecasting is the unprecedented volatility as oil is behaving more like nancial markets than a commodity. The chart below shows that for decades, oil moved in modest ranges with large fluctuations only occurring in case of war or OPEC embargo. Over the past decade, oil has seen movements in the 10- 20% range just on minor news. This means when oil demand eventually catches up with production, there is a high likelihood that markets will react violently, pushing oil well above our forecasted targets.

CHINA: SLOWDOWN TO CONTINUE, BUT NO HARD LANDING

China’s rate of growth will decline to 6.5% in 2016, down from 10.4% in 2010, but it will remain among the largest contributors to global growth. Every year, 30 million people are added to China’s middle class, increasing demand on cities, roads and power grids, all of which require enormous infrastructure spending. Last year, China consumed more coal than the rest of the world combined and imported 70% of the world’s seaborne iron ore. In 2012, China accounted for half of the global growth in oil demand. That is why a slowdown in the world’s biggest commodity consumer will have a great impact worldwide.

“China has financial weaknesses, to be sure, […] but there is little reason to question the government’s capacity to intervene if something goes seriously wrong, particularly given the country’s nearly $3.5 trillion in foreign exchange reserves.”

Barry Eichengreen,

George C. Pardee and Helen N. Pardee Professor of Economics and Political Science, University of California, Berkeley

China faces three challenges. First, growth has historically been led by exports. With a slower global economy and rising wages making China less competitive, the 10% per annum annual rise in exports is not sustainable.

Second, China’s property market shows signs of massive oversupply. The country’s unsold home inventory hit a record of 686 million square metres at the end of October, which is almost 70 million homes, up 17.8% from the previous year. Property prices fell for 18 months straight before stabilizing as the government took steps to stimulate the mortgage market.

“The big challenge for China is that it has to reform everything at the same time. From an export-led economy to a consumer-driven one. From state-owned enterprises dominating to the private sector taking over. From a state-controlled nancial system to market-driven banks. From a pegged currency to an open capital account. This is a tall order.”

Mark Zandi,

Chief Economist, Moody’s Analytics

Third, China’s growth has been fuelled by astonishing growth in credit. McKinsey estimates that China’s total debt has nearly quadrupled, reaching $28 trillion in 2014, up from $7 trillion in 2007. China’s debt is 282% of GDP and is larger than that of the United States or Germany. Half of all loans in China are linked to its overheated real estate market.

China’s economy has signicant vulnerabilities but incredible potential, particularly as the consumer gains strength and confidence. China’s household savings rate is a staggering 32%, with many consumers saving more than half their income. This sounds quite alien to Canadians, where the savings rate is barely 2%. But, as China’s government builds up the social safety net and consumers gain confidence, that savings rate can come down. If just a small portion of the current savings were channelled into spending, the economic boost from consumption would be enormous.

Based on our research, we are forecasting that China’s GDP will grow 6.5% this year and 6% in 2017. This represents a slowing but not a crash. In part, this is because China’s government still has various tools to enable it to stimulate the economy. We expect China will continue to lower interest rates in 2016 and that it will see modest depreciation of the renminbi. While the RMB is loosely pegged to the U.S. dollar, currently one of the world’s strongest currencies, a 10% depreciation would push China all the way back to where it was in 2011.

During the Crystal Ball Symposium, Robert Fowler (left) and Martin Ford addressed two important issues to Canadians: the future of work in an era of rapid technological progress and the future of the world in the face of political instability and terrorism. Nov. 30, 2015, Ottawa.

THE CANADIAN DOLLAR: WEAKER IN 2016, BUT PICKING UP IN 2017

The loonie is expected to average $0.71 in 2016 before rising to $0.74 next year, as continued weakness in oil prices and other commodities will put downward pressure on the currency.

More importantly, the gap in interest rate expectations between Canada and the United States will expand in 2016. The U.S. Federal Reserve raised interest rates by 0.25% on December 16, 2015, and we expect three more 0.25% increases to take place this year, bringing U.S. interest rates up to 1% by the end of 2016.

In stark contrast, the market does not expect any interest rate increases in Canada this year. In fact, the Governor of the Bank of Canada spoke in December about negative interest rates and other unconventional monetary policies, explaining that these could be an option if needed. As a consequence, investors foresee rising returns in the United States compared with a fl at or a negative outlook in Canada. This, combined with a rising awareness of Canadian vulnerabilities in housing and consumer debt, has led to market pessimism about the loonie.

THE BOTTOM LINE FOR CANADIAN BUSINESS

Canadian exports fell by only 1% in 2015 despite the gaping hole left by the fall in energy prices. The oil and gas sectors amount to 24% of Canadian exports, and, with prices falling by half, this amounts to a 12% hit to Canada’s international sales. In addition, there are suppliers and service providers all across Canada that depend on the energy industry and many of them are struggling.

“Far from a warning of danger, recent volatility is a clear sign that growth is back and on a broader base. Canada is already capitalizing and is expected to build on 2015’s success into 2016 and through the medium term.”

Peter Hall,

Vice President and Chief Economist,

Export Development Canada

However, our members told us that there are enormous opportunities in the resurgent U.S. economy and with Europe’s recovery gaining traction. With the dollar at the lowest level in 11 years, Canadian export prices are highly competitive and translating into stronger margins for many products.

In fact, we have already seen astonishing growth in Canada’s manufactured exports and services. The auto sector grew by a booming 14% in 2015, and technology exports gained 13% while aerospace soared by a whopping 29%. Export Development Canada, the institution with the best track record in forecasting Canada’s international sales, expects that export growth will reach 7% next year, a healthy gain.

Overall, the Canadian economy grew by a paltry 0.9% in 2015, and we are forecasting a 1.5% rise in 2016 followed by a 1.8% gain next year. In the midst of a soft domestic economy with weakness in consumption and housing, the most important source of growth will come from exports. Indeed, the forecast is predicated on strong export performance by Canadian companies. However, for growth to continue, Canada must improve its productivity and competitiveness.

EDC Export Forecast

Sector |

C$ billion | % of total exports | Export growth (%) | ||

|---|---|---|---|---|---|

| 2014 | 2014 | 2014 | 2015 | 2016 | |

| Agri-food | 56.2 | 9.6 | 12.0 | 8 | 3 |

| Energy | 142.3 | 24.2 | 14.9 | -31 | 17 |

| Forestry | 32.5 | 5.5 | 9.1 | 6 | 4 |

| Chemical and Plastics | 41.6 | 7.1 | 12.5 | 8 | 7 |

| Fertilizers | 6.9 | 1.2 | -11.4 | 36 | 2 |

| Metals, Ores and Other Industrial Products | 73.2 | 12.5 | 8.0 | 4 | 7 |

| Industrial Machinery and Equipment | 30.6 | 5.2 | 9.6 | 10 | 5 |

| Aircraft and Parts | 14.5 | 2.5 | 28.7 | 29 | 17 |

| Advanced Technology | 14.6 | 2.5 | 5.5 | 13 | 5 |

| Motor Vehicles and Parts | 67.9 | 11.6 | 8.7 | 14 | 5 |

| Consumer Goods | 7.7 | 1.3 | -3.8 | 27 | 4 |

| Total Goods | 492.1 | 83.8 | 11.0 | -2 | 8 |

| Total Services | 95.4 | 16.2 | 3.0 | 2 | 4 |

| Total Exports | 587.5 | 100.0 | 9.6 | -1 | 7 |

For details, please go to www.edc.ca/EN/Knowledge-Centre/Economic-Analysis-and-Research/Pages/globalexport-forecast.aspx

THE CRYSTAL BALL SYMPOSIUM: The Biggest Challenges Facing Canada and the Global Economy

On November 30, 2015 in Ottawa, our second annual Crystal Ball Symposium brought together corporate and government leaders to delve into the big trends that are affecting Canadian business.

In a remarkable evening of presentations and debate, experts addressed two of the biggest challenges facing Canada and the global economy. The rst presentation was on technology and the future of work and featured Martin Ford, the founder of a Silicon Valley-based software development firm and the author of the best-selling Rise of the Robots: Technology and the Threat of a Jobless Future. The second presentation was an analysis of the political risks of terrorism and mass migration by Robert Fowler, a distinguished retired Canadian diplomat and public servant.

In the presence of Canada’s top public servants and the leadership of the Canadian Chamber of Commerce, our expert guests sketched the challenges in the years ahead, which are perilous but also hopeful.

Crystal Ball Symposium, Nov. 30, 2015, Ottawa.

Featured Speakers

Martin Ford

Martin Ford

Author, Rise of the Robots: Technology and the Threat of a Jobless Future

Martin Ford is the founder of a Silicon Valley-based software development firm and the author of two books: New York Times bestselling Rise of the Robots: Technology and the Threat of a Jobless Future and The Lights in the Tunnel: Automation, Accelerating Technology and the Economy of the Future. In Rise of the Robots, Martin Ford looks at how the accelerating pace of new technologies will change, for better and worse, the economy, the job market, the education system and society at large.

Mr. Ford has over 25 years of experience in computer design and software development and holds a computer engineering degree from the University of Michigan, Ann Arbor and a graduate business degree from UCLA. He has written for publications including Fortune, Forbes, The Atlantic, The Washington Post, Project Syndicate, The Hufngton Post and The Fiscal Times. He has also appeared on numerous radio and television shows, including programs on NPR and CNBC.

Robert R. Fowler, O.C.

Robert R. Fowler, O.C.

Distinguished diplomat and public servant

During his 38 year public service career, Robert Fowler was Foreign Policy Advisor to Prime Ministers Trudeau (Pierre), Turner and Mulroney, Deputy Minister of National Defence and Canada’s longest serving ambassador to the United Nations. He was ambassador to Italy and three UN food agencies, sherpa for the Kananaskis G8 Summit and the personal representative for Africa of Prime Ministers Chrétien, Martin and Harper. He retired from the federal public service in 2006 and is now a senior fellow at the University of Ottawa’s Graduate School of Public and International Affairs. He was appointed special envoy to Niger in 2008. While acquitting his UN mission, Mr. Fowler was captured by al Qaeda and held hostage in the Sahara Desert for 130 days. To this day, he remains an outspoken advocate of the importance of foreign policy and Canada’s engagement with Africa.

CRITICAL ISSUES IN THE YEARS AHEAD: ARE ROBOTS A REAL THREAT TO EMPLOYMENT?

The middle class has always depended on job creation and rising wages in order to improve its standard of living. More than ever, astonishing advances in articial intelligence (AI) and robotics have the potential to threaten that prosperity by displacing large parts of the labour force. The debate focuses on how large a problem this may become for the labour market and whether workers can adapt. Moreover, it is no longer just the lowest skilled jobs that can be automated (e.g. cashiers replaced by kiosks or drivers replaced by autonomous vehicles). Software is able to do tasks previously reserved for the middle class with programs doing the work of bookkeepers, lawyers and journalists. Estimates suggest between one-third to one-half of all jobs might be automated over the next decade in the U.S.

However, many are sceptical about such predictions because so many alarms have been raised in the past. Indeed, the one constant of economic growth in the past two centuries is that creative destruction has replaced countless less efficient industries with new technology, yet massive disruptions have failed to occur. Labour markets have adjusted so there is no need to lament the candle makers who lost out to the light bulb or the typists who were shunted aside by desktop computing.

However, there is now an emerging consensus that we are headed into a new era that we have not seen before. Technological advancement is accelerating, and there is evidence that “this time is different” because of the decrease in the number of hours worked in the U.S. Over the 15-year period between 1998 and 2013, there was no growth at all in that number even though output grew and the U.S. population grew by 40 million people, according to the U.S. Bureau of Labor Statistics.

While the intersection of technology in the economy is historically the source of productivity gains, Martin Ford argues that three technological trends are creating a scenario for far fewer jobs in the future.

First, Moore’s Law regarding the doubling of computer processing power every two years has not abated. In fact, there seems to be a sustained exponential acceleration of processing power for which we may not be prepared.

Second, machines are now taking on cognitive tasks. They can think and solve problems and, most importantly, they can learn. With machine learning and smart algorithms, they can make predictions. Since large numbers of people do relatively predictable actions in their jobs, this implies that large numbers of jobs are susceptible to replacement by machines.

The third trend is that information technology (IT) is now truly general purpose in nature. It is ubiquitous, and there is no safe haven for workers. Across the entire economy, IT will make everything less labour-intensive. Equally signicant is the fact that new industries are not nearly as labour-intensive as traditional industries. As a result of technology, business is producing more with fewer workers, and U.S. statistics show that every decade produces fewer jobs than the previous one.

Major changes in the numbers and types of jobs means that the skills mismatch will exacerbate. The kinds of jobs that will be created will not be accessible to the average worker with a typical education and skills. Education and training by themselves will no longer be a solution, according to Mr. Ford. While post-secondary graduates do better than those who only finished high school, that is true because the job situation is in collapse for those without a degree or credential, he explained.

Robots have been around for a long time, replacing rote and repetitive jobs in manufacturing, for example. More recently, however, automation is extending beyond blue collar jobs to white collar jobs in finance and law. It is predicted to encroach on more knowledge jobs in the future.

AI’s and robotics’ impact on jobs has important ramications for the economy and for the capitalist system where it is critically important for people to have purchasing power. If jobs go away or if they do not provide sufficient income, there is a risk of a deflationary scenario in our economy. Meanwhile, profits are coming from efficiency improvements, but protability is not coming from selling more items. Eventually, that will have to change and sales of more items will be necessary.

The evaporation of many jobs may demand a decoupling of jobs from income. Today, you have an income if you have a job, but, in the future, we may want people to have access to some income even if they do not have a job. Mr. Ford believes we need to begin to debate potential solutions to this evolution of innovation and much weaker job creation.

New Industries Are Less Labour Intensive |

|

|---|---|

| General Motors (1979) | Employees 840,000 Revenue $11 billion (Infl ation adj. 2012$) |

| Google (2012) | Employees 38,000 Revenue $14 billion |

RISING POLITICAL RISK: MIGRATION, TERRORISM AND THE BUSINESS RISK CALCULUS

Canadian businesses have succeeded in diversifying globally, penetrating new markets and expanding their export orientation. But for international businesses and governments alike, the political risks have never been greater. The world is in a perilous state, and there is no shortage of daunting challenges.

Robert Fowler argues that threats from political instability, massive migration and terrorism, together, pose a greater threat to our society than economic weakness.

European politics are in turmoil as a result. Mr. Fowler believes that migration alone could well destroy the European project. This migrant crisis was in the cards for decades but only the scale was unpredictable. The numbers are staggering: between January and early December 2015, 868,000 migrants arrived by sea in Europe, compared to 23,000 who arrived in 2012. Ten years ago, there were 38 million displaced people globally, but, today, the number is about 60 million due to the wars of the Middle East.

Massive migration will continue unabated, in Mr. Fowler’s view, as “one billion Africans will not watch their children starve if there are alternatives.” Many international observers are seeing migration and jihadi terrorism as the new normal. The juxtaposition of these two crises is daunting nonetheless.

“The scale of migration is utterly unprecedented and it is occurring at a time of more aggressive strength of jihadi terrorism.”

Robert Fowler,

distinguished Canadian diplomat and public servant

This is not just a Syrian and Middle Eastern issue. It is an issue that is poisoning European politics, and, when one considers the Republican Party dialogue, it is also poisoning American politics. “What we are experiencing now will change our country,” says Mr. Fowler. “We want that change to be positive.”

Where is the good news in this bleak outlook? Our world is healthier, safer and richer, and Mr. Fowler believes we ought to make that work for us. He cautions that in the business community as well as in government, it will mean that if you cannot take the long view and take the big risk, you will not want to be in the game.

The Power to Shape Policy & Of Our Network

Get plugged in.

As Canada’s largest and most influential business association, we are the primary and vital connection between business and the federal government. Wtih our network of over 450 chambers of commerce and boards of trade, representing 200,000 businesses of all sizes, in all sectors of the economy and in all regions, we help shape public policy and decision-making to the benefit of businesses, communities and families across Canada.

For more information, please contact:

Hendrik Brakel | Senior Director, Economic, Financial & Tax Policy | 613.238.4000 (284) | hbrakel@chamber.ca

Chamber.ca | CanadianChamberofCommerce | @CdnChamberofCom