[Download the report as a PDF]

ABOUT THE ONTARIO CHAMBER OF COMMERCE

For more than a century, the Ontario Chamber of Commerce has been the independent, non-partisan voice of Ontario business. Our mission is to support economic growth in Ontario by defending business priorities at Queen’s Park on behalf of our network’s diverse 60,000 members.

From innovative SMEs to established multi-national corporations and industry associations, the OCC is committed to working with our members to improve business competitiveness across all sectors. We represent local chambers of commerce and boards of trade in over 135 communities across Ontario, steering public policy conversations provincially and within local communities.

Through our focused programs and services, we enable companies to grow at home and in export markets. The OCC provides exclusive support, networking opportunities and access to policy insight and analysis to our members. We also work alongside the Government of Ontario on the delivery of multiple programs, and leverage our network to connect the business community to public initiatives relevant to their needs.

![]()

The OCC is Ontario’s business advocate.

Author: Reid McKay, Economic Analyst

Designer: Sarah Fordham RGD, Senior Designer

ISBN: 978-1-928052-57-9

©2019. Ontario Chamber of Commerce. All Rights Reserved.

TABLE OF CONTENTS

Glossary

Introduction

Defining Ontario’s Sub-Sovereignty

Provincial vs. Federal Debt

Ontario’s Financing Costs

Ontario’s Fiscal Prudence

Government Revenue Generation

External Factors

The Business Perspective

Conclusion

References

GLOSSARY

ABSOLUTE VALUE

Absolute value refers to the actual magnitude of a numerical value or measurement, irrespective of its relation to other number or values.

BOND YIELD SPREAD

The difference in investment return offer by two different bonds.

DEAD-WEIGHT LOSS

Non-recoverable capital.

DEBENTURE

A debt instrument which is unsecured by an asset.

DEBT INSTRUMENT

A contract or electronic obligation that enables the issuing party to raise funds by promising to pay a lender in accordance with the terms of the contract.

DEBT PRIVILEGES

The ability of a lender or borrower to exercise certain privileges, such as refinancing (i.e., debt rollover).

DEBT ROLLOVER

Also referred to as refinancing, ‘rolling over debt’ refers to a borrower’s choice to simply keep paying interest payments for a specified period of time, and to repay the principle of the debt at a later specified time.

DEBT VALUATION

The processes, and information used to understand and quantify debt.

INSOLVENCY

A situation in which a debtor is unable to pay its creditors.

MARGINAL WELFARE COST

The added negative impact an additional tax, or other incremental societal cost, which must be shouldered by an economy.

MORAL HAZARD

Moral hazard arises when a party becomes less risk averse due to an understanding that it will ultimately be sheltered from the consequences of taking such risks. An example may be a driver who becomes more reckless once under the protection of a more robust auto insurance policy.

NOMINAL GROWTH RATE

The growth rate of an economy, as often measured by GDP, without adjustments for inflation.

NORMATIVE

A standard behaviour inherent to a norm that is often referenced to give justification to a prioritization of goals (e.g. “investors would be wise to borrow when interest rates are low”).

OPPORTUNITY COSTS

The loss of potential gain from other alternative investments when one alternative is chosen (e.g. if choosing to purchase a sedan over a pickup truck, the opportunity cost would be the future inability to transport large amounts of cargo).

ORGANIC REDUCTION OF DEBT

The reliance upon increasing government revenue, by way of economic growth, to pay down debt, or stem the perpetual increase of debt.

SUPERIOR-GRADE CREDIT RATING

Refers to a borrower with an exemplary credit rating (e.g. between AAA and AA-, S&P, superior-grade), and therefore suitable for investment lending.

INTRODUCTION

Discourse surrounding Ontario’s debt is a contentious topic, with views ranging from its characterization as a ‘crisis’ requiring immediate action, to suggestion that deficit spending is necessary to spur economic growth. A long-standing issue for Ontario’s business community, the Ontario Chamber of Commerce’s 2019 Business Confidence Survey[1] found that nearly 80 percent of respondent businesses are concerned about the impact the provincial debt could have on Ontario’s economy.[2] They believe the Province’s fiscal health directly impacts the ability of businesses to be competitive and capitalize on opportunities in growing industrial sectors.

At over $348 billion, or approximately 41 percent[3] of provincial GDP,[4] Ontario’s debt load is considerable and often difficult to contextualize. When combined with the federal debt (approximately $680 billion[5]), the debt-to-GDP ratio for Ontarians nears 80 percent. Such a high debt can weigh heavily on economic growth, as future generations may struggle to meet financing payments they had little influence over. Conversely, failing to make critical investments in infrastructure and services now may have significant costs, as Ontario’s future economy may struggle to compete with others replete with robust public infrastructure and services. Faced with a slowing economy and the possibility of interest rates lifting off from historically low levels, the Ontario government is currently placed at a critical juncture that will impact generations to come: does it embark on a debt repayment schedule that could hinder future economic growth, or does it continue making investments in the hope that economic growth will outpace growing debt financing costs?

In December 2018, the Financial Accountability Office of Ontario (FAO) estimated Ontario’s net debt would rise by approximately $46 billion per year, reaching an unprecedented $450 billion by 2022-23,[6] amounting to just over $28,000 per Ontarian. Importantly, Ontario’s debt-to-GDP ratio is also expected to rise roughly 4 percentage points to 45.2 percent in 2022-23.[7] Fiscal challenges of the magnitude Ontario is faced with are usually the exclusive domain of national governments, which retain prerogative over powerful tools such as monetary policy to help manage debt. While federations such as Canada’s are uncommon in the world, there are arguably none which ascribe as much responsibility to their sub-sovereign governments (SSGs)[8], such as Ontario. Costly and complex responsibilities placed within the Ontario government’s jurisdiction, such as health care, typically rest within the purview of a national government, if at all, in most other nations.[9] In considering how to best steward its debt, the Ontario government must therefore reconcile a vast array competing responsibilities placed under its purview, with the limited number of policy levers placed within its capacity as a province. Within the framework of the business case for improved debt and deficit management, this report examines how the tenets of debt valuation[10] and economic growth could come to balance in Ontario’s unique situation. It also explores how the Ontario government could retain debt as a valuable tool to ensure the province gets the highest return on taxpayer dollars.

DEFINING ONTARIO’S SUB-SOVEREIGNTY

When SSGs, such as Canadian provinces, look to debt markets to secure capital for deficit spending through the sale of a debt instrument (such as a bond or debenture)[11], the market decides the requisite interest rate a government must pay for a given amount of debt. Principles, which are critical to assessing a borrower’s creditworthiness (often simply referred to as ‘fundamentals’), can be expected to dictate borrowing conditions, like interest rates and borrowing privileges.[12]

Such fundamentals often include, but are not limited to:

- The perceived ability of the borrower to repay the debt;

- The amount of debt being sold in comparison to the borrower’s current debt load; and

- The borrower’s history of prioritizing debt obligations (i.e., creditworthiness).

Normally, the degree of scrutiny by which debt fundamentals are applied to an SSG’s borrowing request also depends on the perceived ability or willingness of the sovereign government to intervene if dire circumstances arise for the SSG. In the case of Canada, this refers to the ability of the federal government to intervene on behalf of a provincial government. The interest paid by SSGs to borrow money can, therefore, be either adversely or favourably affected by how the sovereign government chooses to support its SSG’s spending habits. While a history of bailing out other SSGs or prior commitment to supporting an SSG’s debt have been shown to provide favourable lending conditions to the SSG, doing so can have an adverse effect on the sovereign government’s ability to market debt, and, in some cases, provide SSGs an incentive for moral hazard.[13]

When deciding the degree by which to apply lending fundamentals to an SSG’s debt instrument, creditors have been known to consider everything from historical precedent, such as bailouts and stated commitments, to tacit verbal acknowledgment of a sovereign government’s accountability for SSG debt. This makes investments in SSG debt instruments a more speculative undertaking, as creditors must consider the degree to which the sovereign government will support the SSG, and how the sovereign government’s creditworthiness compares to that of the SSG.

Ontario’s Unique Situation

Ontario’s GDP is nearly $850 billion, by far the largest of the provinces, and comprises nearly half of Canada’s GDP. While Ontario undoubtedly benefits from its relationship with Canada, the degree to which Canada is capable of aiding Ontario in the event of an economic downturn is limited due to its sheer size. This uneven relationship raises a unique question: what happens if the sovereign government is not only responsible for, but dependent on, the SSG?

Ontario is, therefore, in an exceptional situation; it has the debt exposure of a sovereign government but is left without the generous lending fundamentals usually provided by a federation or monetary union. In addition to being tasked with maintaining and growing the strength of the economic engine the rest of Canada relies upon, Ontario must do so absent the financial shelter of the federal government. Ontario is beholden to numerous creditors which could overwhelm the Bank of Canada with ease should our province be unable to appease creditors in a debt crisis. Simply put, the Ontario government must work outside the support of the national government and central bank to drive economic growth.

Instead of comparison to other sub-sovereigns, such as American states or other Canadian provinces, a more suitable comparison for Ontario may be a relatively strong sovereign government tied to a monetary union with other sovereign nations. Like Ontario, such sovereign governments have significant control over economic factors and provide critical public services. Akin to the economic dependency of Canada on Ontario, nations within a monetary union tend to rely heavily upon a single member for monetary guidance. With this in mind, an appropriate comparison for Ontario may be Germany or France. As two of the strongest nations within the European Union (EU), Germany, and France have significant influence over how key economic policy tools are used, such as monetary policy and financial relief (e.g. bail-out packages). Taken from this perspective, Ontario’s current debt-to-GDP ratio of 41 percent[14] seems less egregious when compared to Germany (64 percent), France (97 percent), and other European strongholds such as Belgium (105 percent).

The European Union Analogy

The EU’s 2014 debt crisis provides a precedent to observe the fall-out of a financial crisis in a monetary union (i.e., the euro). Faced with the possibility of economic collapse during the crisis, financially distressed countries (such as Greece) managed to save their economy by accepting large financial bailout agreements offered by the European Central Bank. While acceptance of these bailout agreements meant imposing strong restrictions on Greece’s discretionary spending, it also allowed Greece to retain use of the euro and maintain critical access to generous lending fundamentals.

Greece’s acceptance of the agreement offered by the European Central Bank demonstrated Germany’s central role in management of the euro and EU fiscal policy. As the largest economy in the monetary union, Germany’s direction in assessing the debt crisis proved central to brokering the agreement. Had the agreement failed, the euro’s future would have been more unclear, as the future of other distressed EU countries would remain uncertain in absence of the precedent for a bailout. In turn, this would have adversely affected the borrowing fundamentals of all members of the monetary union. If Greece had defaulted or been unable to attain a bailout from the European Central Bank, it would have likely needed to abandon the euro in favour of its prior domestic currency to obtain financing critical to the preservation of the country (albeit at extremely high-interest rates).

For Ontario to maintain preferential borrowing rates and a commensurate credit rating, the provincial government must consider the strength of its neighbouring provinces’ economies with which Ontario is inseparably tied. As neighbouring provinces experience similar if not higher provincial debt-to-GDP ratios, Ontario must use its influence and size to ensure the Canadian federation doesn’t face the same challenges to that of the EU. The Ontario government would be wise to understand how the plight of other provinces affects its economy as well as how creditors view the province’s economy within the broader Canadian federation. Taking pre-emptive action to improve conditions for interprovincial trade and the ability for individuals to move freely amongst cities and provinces has been instrumental to improving the European economy and would likely do the same for Canada.

PROVINCIAL VS. FEDERAL DEBT

Ontario’s economic prominence within Canada means the success of other provinces and their ability to issue debt at favourable rates is influenced by the health of Ontario’s economy. If Ontario’s economy is doing poorly, other provinces will suffer in their ability to sell debt as the Canadian economy will have limited capability to offer support should the other province require it. Similarly, if Ontario’s economy is doing well, creditors can take comfort in knowing that if a province begins to struggle, agreements (such as the Interprovincial Transfer Agreement) will be able to assist in mitigating economic woes.[15] Therefore, due to the interconnected nature of the provinces (in that they collectively drive the value of the Canadian dollar and economy), the largest provinces naturally have the greatest influence over the collective health of the Canadian economy.

To ensure the economic relationship between provinces and the federal government are not abused, the agreements that define the confines of the relationship must be infallible. These agreements provide provinces with agency over their fiscal policy by removing subjectivity over when and how a province may be expected to provide or receive economic relief to and from other provinces.

The strength of these agreements impacts how creditors evaluate the debt fundamentals of individual provinces. If a province feels they will be supported regardless of their fiscal prudence, they will be prone to make unwise or overly ambitious borrowing decisions (similar to Greece prior to the EU debt crisis). This moral hazard could harm other provinces within Canada, as they will not be able to predict when their resources will be tapped to aid neighbouring provinces.

Maintenance of long-standing transfer payment agreements are central to the preservation of how debt fundamentals are applied to the credit rating of both Ontario and Canada. Changing how aid is allocated amongst provinces could adversely affect not only the federal government’s credit rating, but the credit ratings of provinces, such as Ontario, which maintain higher ratings than that of the provincial and territorial average. Canada’s use of an algorithm to dictate transfer payment allocation removes any kind of political subjectivity and provides creditors a reliable metric to measure how and when a province will receive aid. The transfer payment system also assigns agency and responsibility to each province over measures taken to finance debt and deficit spending. In attempt to avoid any creditor speculation, or risk of moral hazard and excessive spending as suffered by the EU during the debt crisis, Canada has reaffirmed its commitment to not provide sub-sovereign governments with bailouts on many occasions.

While many of Ontario’s municipalities maintain significant debt, they are all at a net value of zero. This is because Ontario municipalities are only allowed to borrow against capital projects which subsequently increase the asset holdings of the city. Unlike the provinces or country, municipalities are not allowed to sell long-term debt to finance operating expenditures, which by nature allocates little funding to infrastructure development. This restriction limits the ability of municipalities to finance long-term projects as all borrowing must be capitalized.

The agency with which provinces approach debt stewardship and spending is deserving of careful consideration as net provincial debt is soon expected to exceed net federal debt. Our arrival at this critical juncture is without precedent: never have Canadian provinces carried a collectively larger debt than the national government. While some provinces, such as Quebec and Nova Scotia, have worked to alleviate their debt burdens, others have only increased theirs, with Ontario recently suffering a slight credit downgrade due to growing debt and a slowing economy. Reaffirming the responsibilities of each province and better defining the options each province has at their disposal to alleviate debt burdens may provide valued insight as to how the Canadian government can approach efficient and effective debt and economic stewardship.

ONTARIO’S FINANCING COSTS

Now that Ontario’s debt has been situated within a greater context, the value of that debt can be assessed.

Assessing what the absolute value[16] of Ontario’s debt means to Ontarians is impossible without understanding the relative costs of servicing that debt. Valuable metrics such as financing costs and debt-per-capita provide relative measures of the debt’s impact on average Ontarians.

In low-interest rate environments, governments are able to sustain higher levels of debt because the cost of financing the debt is relatively low. The financing cost of Ontario’s debt as of 2018 is approximately eight cents for every tax dollar collected, the lowest in nearly 30 years.[17] While the debt 30 years ago was much lower, the interest rates were comparatively much higher—peaking in the 1990s, when debt financing payments reached 15.5 cents per dollar collected. In examining the past ten years, we can see that despite having the second largest net financial debt-per-capita in Canada, Ontario has maintained below average percapita financing costs (Figure 1).

A recent report by Olivier Blanchard, Professor of Economics Emeritus at MIT, draws attention to the fact that the nominal growth rate[19] of an economy almost always exceeds the interest rates on government bonds. Blanchard asserts that debt reduction could simply occur by rolling over[20] existing bonds, as tax revenues will organically increase as the economy grows, because the nominal growth rate will always exceed that of the cost to finance debt. This logic is most visible in instances of slow growth or recession when deficit spending offers the most value. To avoid greater economic catastrophe, central banks will often jump-start slow or poor growth using debt instruments that demand returns far less than the negative consequence of non-action. Following the 2008 financial crisis, the Ontario government seized upon low-interest rates intended to stimulate the economy, increasing capital expenditures in an effort to improve the province’s economic prospects.

![Figure 1: Interest Payments by Province, Per Capita [18]](https://gncc.ca/wp-content/uploads/2019/04/figure1_redo.png)

Blanchard[21] goes further in suggesting that deficit spending would instead be most effectively assessed by how the “risk-adjusted social rate of return on public investment” compares to the “risk-adjusted rate of return on private capital.”[22] In essence, he proposes government borrowing be allocated to funding projects and programs expected to deliver a higher return on investment than the interest rate used to finance the project. Canadian economist and Deputy Director of the International Monetary Fund’s Research Department, Jonathan Ostry, suggested that low interest rates are likely to be the norm and as such there is little reason to adopt austerity measures to reduce debt other than for the sake of austerity itself.[23] Recent commentary by the Governor of the Bank of Canada, Stephen Poloz, confirms as much, with Poloz affirming that Canada’s economic outlook “continues to warrent a policy interest rate that us below the neutral range.”[24] With this in mind, the optimal policy to reduce debt might be one which gradually phases in spending cuts or tax increases at a rate that stems the perpetual growth of debt.[25]

Blanchard and Ostry’s viewpoints suggest that maintenance or improvement of the province’s credit rating must be given top priority. If governments begin to show a proclivity for deficit spending—as was the case when Ontario’s credit was downgraded in December 2018—interest rates would increase. The provincial government’s ability to maintain a superior-grade credit rating is an indication of what might be deemed an ‘acceptable’ level of borrowing. Paying close attention to how markets react to fiscal and investment policies can provide governments with valued and timely indication of whether their policies will be effective in advancing the economy. Markets are extremely quick to react to changes in spending and borrowing, raising interest rates and decreasing credit ratings when appropriate, which makes the risk of an unforeseen credit crisis negligible. Notably, the European debt crisis arose more from stagnant growth and excessive operational spending than it did heightened debt levels.

Undoubtedly, Ontario still has wasteful spending to reign in. Though the province has maintained a superior-grade credit rating,[26] the economy has exhibited signs of slowing, and the Bank of Canada is expected to begin a regiment of interest rate hikes.[27] While Ontario has and will enjoy favourable financing rates to fund deficit spending, such rates are capped at the rate received by the Canadian government,[28] which is already less favorable than others within the OECD, such as Germany, Scandinavian countries, and Japan (which maintains a notable 200 percent debt-to-GDP ratio).[29] If Ontario experiences a drastic increase in interest rates (due either to its own inability to maintain economic growth, or that of neighbouring provinces), the consequence could be the Province paying far more than expected to maintain its regime of debt payments, as its ability to rollover existing debt becomes restricted.[30] Increased interest payments on debt will crowd out government’s capacity to spend on programs and services valued by businesses and Ontarian’s alike. Investments in areas such as transit and transportation, broadband internet, health care, skills and education, and trade promotion will help grow the economy and allow businesses to flourish, jobs to be created, and, ultimately, Ontario to be more competitive and prosperous.

ONTARIO’S FISCAL PRUDENCE

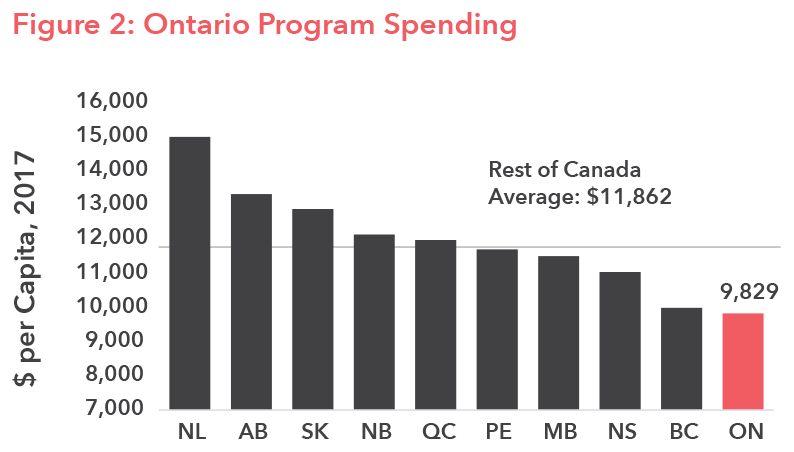

Despite having a large debt, Ontario has exhibited strong fiscal prudence compared to other provinces. In 2017, Ontario only spent an average of $9,829 per capita on programs—the lowest in Canada (Figure 2). Further, spending on programs has grown at half the rate of the rest of Canada.[31]

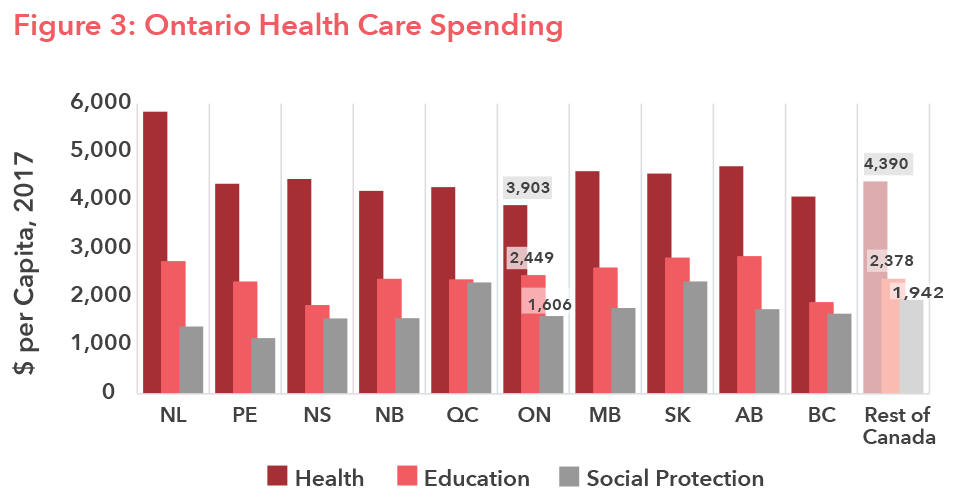

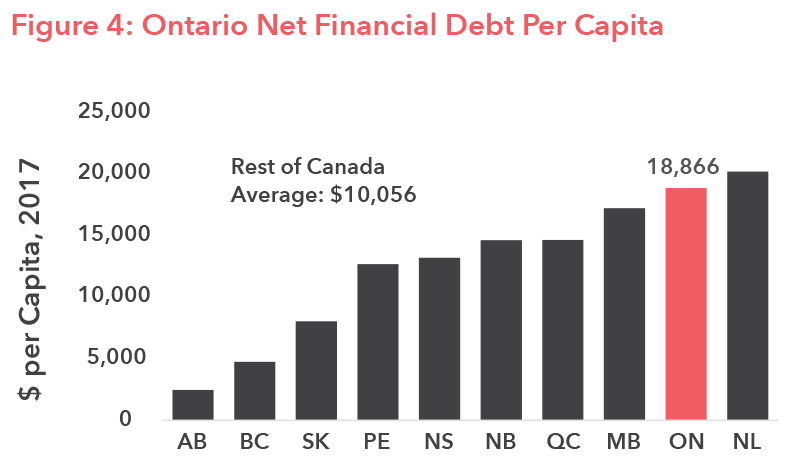

Due to Ontario’s relatively large size, it has been able to realize economies of scale, which have resulted in relatively low per-capita expenditures on health care, education, and social protection (Figure 3).[32] Yet, despite relatively modest spending, Ontario’s per-capita debt and debt load remain high in comparison to other provinces (Figure 4).[33]

In summary, Ontario has done comparatively well to reduce expenditures and mitigate deficit spending costs. As discussed, spending cuts must be done with the full understanding of the economic consequences associated with the failure to either maintain and build critical infrastructure, or invest in social programs and growth-supporting services. It is also worth noting deficit spending that goes towards the development of government assets (such as infrastructure) is viewed by creditors more graciously as the cost of the debt is offset by an increase in total assets, thus mitigating the effect of these investments on net debt.

GOVERNMENT REVENUE GENERATION

When governments increase taxes to satisfy financing demands, they must do so cognizant of the marginal welfare cost[34] a tax increase inflicts on the economy. Though an obvious necessity, taxes distort decisions made by organizations and individuals on investment, savings, and labour expenditures. Therefore, every tax dollar levied imposes a larger, negative impact on the economy than its immediate dollar value—as the dollar would have otherwise been used to multiply value within the economy; this is why taxes are often referred to as dead-weight loss.[35] Importantly, some tax revenue streams have smaller impacts on the economy than others. For example, business and sales taxes are widely understood to have a larger marginal cost to public funds than income tax.[36] As aggregate provincial debt eclipses national debt, it is important the federal government provides provincial governments with tools for revenue generation that offer the economy the most efficient or least distortive methods of levying tax, ensuring the burden of financing the debt is minimized for future generations.

Understanding the opportunity cost[37] an inherited debt burden could have on future generations also needs to be given due consideration when embarking on deficit spending. The future economic conditions that correspond to the maturity dates of long-term government bonds (e.g. 10 and 20 years) is a matter of speculation. This uncertainty is challenging: when entering long-term debt agreements, the government is agreeing to burden future generations with debt without knowing the condition of the economy at the time of the debt’s maturity. In other words, the opportunity cost of allocating a dollar to finance debt in the future is largely unknown.

Not knowing how to quantify the opportunity cost of deficit spending is further complicated in low interest rate environments. The normative effects of low interest rates present opportunities for public investments in projects with a rate of return on investment that exceeds the going interest rate. This leaves little impetus—outside of opportunism and insurance of a lower debt burden in the event of economic downturn—for governments to begin a regiment of debt repayment. As described by Ostry, “the distortive cost of policies to deliberately pay down the debt is likely to exceed the crisis-insurance benefit from lower debt [levels].”[38] This effect is only compounded by political election cycles, which incentivizes politicians to realize short-term gain over long-term stability. Therefore, organic reduction of debt[39] is likely the default option for governments to supplement revenues in a low-interest rate environment.

Government should thus remain aware of how fiscal policies that attempt to hastily reduce debt may affect Ontario’s business community. An aggressive debt repayment schedule that dismisses valued investment opportunities in favour of repaying inexpensive debt can place an unwarranted burden on businesses and hinder their ability to compete and grow, which ironically inhibits the economy’s ability to supply revenue to the government.

EXTERNAL FACTORS

The Ontario government’s ability to manage its debt load will be largely dependent on its ability to garner a greater economic output. Doing so will be dependent on many external factors, such as the exchange rate, market conditions, and relationships with critical trading partners. These factors only serve to add more complexity to a path already fraught with competing interests.

GDP

While national GDP exhibited strong growth, at roughly 2.7 percent per year from 2015 to 2017, the coming years look less rosy. Recently, the Canadian economy has begun to slow, with growth forecasts closer to two percent for the coming years.[40] Of note, in a low growth environment, investments which serve to hasten economic development become more valued, e.g. trade-enabling infrastructure.

Bond Yield Spreads

This sluggish outlook is supported by other observed economic indicators of troubling times: narrowing bond yield spreads[41] and non-residential construction. The narrowing long- and short-term bond yield spread evidences a pessimistic sentiment among investors; as they weaken their outlook for long-term economic prosperity, investors demand smaller long-term bond yields compared to short-term bond yields. Similarly, a slowdown in non-residential construction has been known to indicate an economic slowdown, as companies stall plans to expand.

Canadian Dollar

It is also important to consider how Ontario benefits from fluctuations in the dollar. While many consider a low dollar to be advantageous to Ontario’s economy, such an assertion may be more aptly directed to Canadian resource economies, such as Alberta, than Ontario or even British Columbia. Contrary to popular thinking, a significantly weakened Canadian dollar can harm consumer goods markets and increase import and financing costs for businesses.[42] Many of Canada’s exports utilize raw materials imported from elsewhere, most often from the United States. The cost of such raw materials is dependent on the relative value of the Canadian dollar, wherein a devalued currency decreases the buying power of Canadian businesses in international markets. Coincidentally, in many cases, raw materials, such as commodities, are also priced in American dollars simply because they are easier to tender to the market when priced in a commonly known and held currency. As a result, a devalued Canadian dollar more likely leads to higher input prices. This, in turn, increases the price of finished goods both for export and domestic markets, diminishing both Canada’s and Ontario’s ability to provide market value.[43] Foreign demand for Canadian exports has been shown to exhibit little correlation to the Canadian dollar fluctuation, least of all in the manufacturing sector—Ontario’s mainstay. Instead, the prosperity of Canadian exports has been largely attributed to market demand for Canadian exports and domestic economic health.[44]

Foreign Exchange Hedging

To improve access to debt markets and hedge risks associated with the Canadian dollar, some government agencies—and, to a lesser extent, governments themselves—have looked to borrow in foreign currencies. Though, this also presents a vulnerability, as a weakened Canadian dollar in turn increases debt financing costs, which ultimately costs taxpayers and businesses more. If businesses are unable to act upon opportunities which strengthen the Canadian economy or decrease the trade deficit—two factors amongst many that dictate foreign exchange rates—the cost of financing foreign debt will increase. With significant portions of both Ontario and Canadian government debt being held in foreign currency, maintenance of low foreign currency financing costs is dependent on prudent stewardship of the economy.

THE BUSINESS PERSPECTIVE

It is important the Ontario government ensure its businesses have as many opportunities as possible to compete on the global stage. While deficit spending is not desirable, it is an indispensable tool used by all economies throughout the world to enhance economic prosperity. Assessing when and whether to invest in needed infrastructure and services (such as transportation infrastructure, broadband internet, or skills development) the government must not only consider the present and future value of such an investment as dictated by interest rates, but the value Ontarians could derive from an investment now versus in the future.

Undoubtedly, the additional tax burden needed to finance a growing debt-to-GDP ratio comes at tremendous cost to businesses, many of which are already struggling to maintain or gain foothold in competitive markets. Commitments made by the government to financing debt in the future decreases the economy’s ability to remain agile to market demand. Similarly, future working generations may not be willing or able to shoulder the choices made by past governments as they struggle to meet financing obligations. For businesses, debt and deficit management is tied to their access to talent, which they identify as one of the factors most critical to their competitiveness.[45] Attracting and retaining talent within Ontario will become more challenging over the long term if there are higher taxes, insufficient infrastructure and services, and fewer opportunities here than elsewhere. An economy overburdened by unnecessary dead-weight loss is unable to secure both the talent and capital necessary for businesses to grow and prosper.

Public debt is not merely a concern for large firms with sophisticated financial operations. Small businesses are small in name only; more than 95 percent of businesses within Canada are small[46]—the majority of which operate entirely within Ontario.[47] It is these businesses that are most vulnerable to the tax burden imposed by poor debt management. Small businesses are often stretched by extremely thin profit margins and are unable to shoulder additional costs. As globalization connects businesses with opportunities around the world, small business must contend with a growing number of firms against which they must compete, many of which benefit from government investment and subsidy. These local companies tend to derive great value from government initiatives that aim to develop Canadian and provincial economic opportunities both domestically and internationally, such as skills development and export programmes. Raising taxes or implementing austerity measures to reduce Ontario’s debt burden may, therefore, have the unintended effect of squandering current opportunity to grow Ontario’s economy.

Ontario already received a strong warning in 2018, when its credit received a slight—but alarming—downgrade. Another credit downgrade could prove detrimental to Ontario’s future, as it would be the last stop before the province leaves the “high grade” investment tier. The provincial government must therefore be careful in its choices to embark on future deficit spending and consider how such choices may affect its credit with lenders. Maintenance of a high, superior-grade credit rating not only ensures Ontario’s continued ability to finance needed development projects, but also indicates much needed tacit approval from bond markets that the actions Ontario is taking to grow its economy is well informed. If the government were to embark on a strict regime of debt repayment, creditors may understand such a choice as ill-advised given current expansionary policy being undertaken throughout the globe.

CONCLUSION

As the Ontario government faces an era of uncertain economic growth, it must demonstrate good debt stewardship—avoiding the siren song of austerity and instead running an efficient government with the capacity to invest for growth and development. Though it may not have access to the monetary tools and trade policies reserved for sovereign states, Ontario’s economic prowess within both the national and the global theatre is what begets economic privilege and dictates monetary balance.

Conveniently, the speed at which markets react to fiscal and monetary decisions made by government will always provide immediate and clear disapproval, should Ontario stray off course. Conversely, market indication of missed opportunities to advance economic opportunity by way of investment in infrastructure, education, or health care are obscure at best. Therefore, policymakers must be diligent in assessing the opportunity cost of investing now rather than later.

Ontarians must understand that there is no concrete or tested method by which to value or assess what constitutes an ‘appropriate’ amount of spending or borrowing. In discussing the best course of action, both government and the public must resist defaulting into rhetorical arguments, and instead look to earnestly consider the consequences of various actions. The decisions government makes regarding debt will transcend the political term in which it is in power, having profound effects on the economy for decades to come.

REFERENCES

- The 2019 Business Confidence Survey was given to Ontario businesses which were members of the OCC and/or their local commerce chambers or boards of trade.

- Ontario Chamber of Commerce. 2019. Ontario Economic Report 2019.

- Net of Ontario’s cash and cash-like assets, Ontario’s debt-to-GDP would be approximately 32 percent.

- Ontario Financing Authority. 2018 Ontario Budget Schedule of Debt. https://www.ofina.on.ca/.

- Royal Banks of Canada. March 2019. Canadian Federal and Provincial Fiscal Tables. http://www.rbc.com/economics/economic-reports/pdf/canadian-fiscal/prov_fiscal.pdf.

- Financial Accountability Office of Ontario. December 2018. Economic and Budget Outlook, Fall 2018. https://www.fao-on.org/en/Blog/Publications/EBO-fall-18#Borrowing%20and%20Net%20Debt.

- Ibid.

- The tiers of government which lay below the ultimate governing body or national government.

- Organization for Economic Co-operation and Development (OECD). 2016. Subnational governments around the world Structure and finance. https://www.oecd.org/regional/regional-policy/Subnational-Governments-Around-the-World-%20Part-I.pdf.

- The processes and information used to understand and quantify debt.

- As compared to a bond, a debenture refers to a loan that is unsecured and backed by general credit alone.

- Debt privileges may refer to a debt instrument’s ability to be rolled over or called.

- Moral hazard arises when a party becomes less risk averse due to an understanding that it will ultimately be sheltered from the consequences of taking such risks. An example may be a driver who becomes more reckless once under the protection of a more robust auto insurance policy.

- Canada’s debt to GDP is currently 77 percent.

- Beck, R., Ferrucci, G., Hantzsche, A., & Rau-Goehring, M. 2017. “Determinants of sub-sovereign bond yield spreads—The role of fiscal fundamentals and federal bailout expectations”. Journal of International Money and Finance.

- Absolute value refers to the actual magnitude of a numerical value or measurement, irrespective of its relation to other number or values.

- Statistics Canada, CANSIM Table 10-10-0017-01, 36-10-0314-01.

- Statistics Canada, CANSIM Table 10-10-0017-01.19.

- Nominal growth rate refers to the growth rate of an economy, as often measured by GDP, without adjustments for inflation.

- Also referred to as refinancing, ‘rolling over debt’ refers to a borrower’s choice to simply keep paying interest payments for a specified period of time, and to repay the principle of the debt at a later specified time.

- Blanchard, O. J. 2019. Public Debt: Fiscal and Welfare Costs in a Time of Low Interest Rates.

- Private capital in this context referrers to the “safe rate” or return on sovereign bonds.

- Ostry, M. J. D., Ghosh, M. A. R., & Espinoza, R. A. 2015. When should public debt be reduced?. International Monetary Fund.

- Governor Stephen Poloz. April, 2019. Turbulent Times for Trade. Bank of Canada.

- Furman, J., & Summers, L. H. 2019. Who’s Afraid of Budget Deficits: How Washington Should End Its Debt Obsession. Foreign Affairs.

- Refers to a borrower with an exemplary credit rating (e.g. between AAA and A), and therefore suitable for investment lending.

- Reuters. October 30, 2018. Bank of Canada will keep raising interest rates, Stephen Poloz says. https://business.financialpost.com/news/economy/bank-of-canada-will-keep-raising-interestrates-stephen-poloz-says.

- Gaillard, N. 2009. The determinants of Moody’s sub-sovereign ratings. International Research Journal of Finance and Economics.

- Investing.com. World Government Bonds. https://ca.investing.com/rates-bonds/world-government-bonds.

- If interest rates rise, governments and corporations may have to re-finance existing debts at higher interest rates. This is most often referred to as rollover risk.

- Financial Accountability Office of Ontario (FAO). Feb 2019. Comparing Ontario’s Fiscal Position with Other Provinces. https://www.fao-on.org/en/Blog/Publications/inter-provcomparisons-feb-2019.

- Ibid.

- Ibid.

- The added negative impact an additional tax, or other incremental societal cost, which must be shouldered by an economy.

- Dead-weight loss refers to non-recoverable capital.

- Organization for Economic Co-operation and Development (OECD). Sept 5, 2015. Taxation of SMEs in OECD and G20 Countries.

- Opportunity cost refers to the loss of potential gain from other alternative investments when one alternative is chosen.

- Ostry, M. J. D., Ghosh, M. A. R., & Espinoza, R. A. 2015. When should public debt be reduced?. International Monetary Fund.

- The reliance upon increasing government revenue, by way of economic growth, to pay down debt.

- Royal Bank of Canada (RBC). 2019. More Room to Grow for All Provinces in 2019. http://www.rbc.com/economics/economic-reports/provincial-economic-forecasts.html.

- A bond yield spread refers to the difference in investment return offer by two different bonds.

- Philip Cross. 2014. The Economic Consequences of a Low Dollar. Frasier Institute. https://www.fraserinstitute.org/sites/default/files/economic-consequences-of-a-lower-canadian-dollar.pdf.

- The effect of this disadvantageous relationship is only compounded by Canada’s balance of trade, which has been firmly in the negative since 2008, meaning Canada imports more goods

than it exports. - Philip Cross. 2014. Weaker Loonie Hurts Canadians More Than It Helps. Frasier Institute. https://www.fraserinstitute.org/sites/default/files/weaker-loonie-hurts-canadians-more-than-it-helps.pdf.

- Ontario Chamber of Commerce. 2019. Ontario Economic Report 2019.

- Defined as fewer than 100 employees.

- Statistics Canada, CANSIM Table 33-10-0105-01.